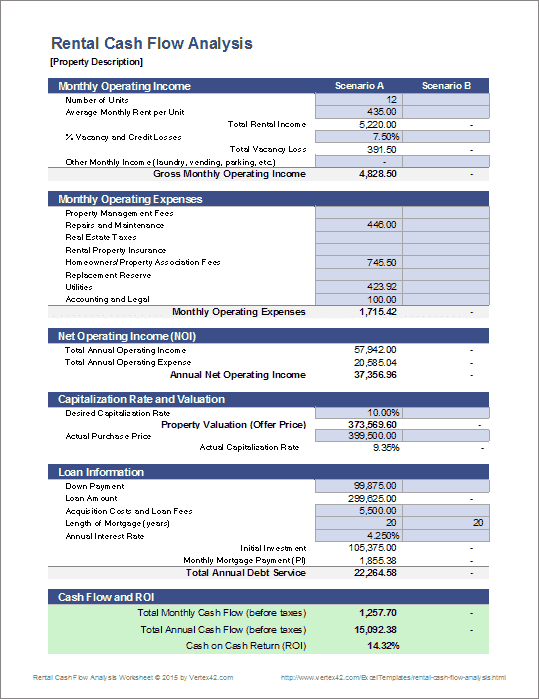

💵 Rental Cash Flow & Profit Calculator

A rental property can look great on the surface, but the real question is what happens after the numbers are added up. Before moving forward, it helps to compare expected rent against financing, taxes, insurance, maintenance, vacancy, and other monthly costs.

This page helps South Jersey buyers and investors estimate rental cash flow, review the most important expense categories, and better understand whether a deal fits their investment goals.

🔎 What Goes Into Rental Cash Flow?

Rental cash flow is not just about what a property rents for. The real picture comes from comparing income against the full set of monthly costs that affect ownership and performance.

🏠 Rent Collected

Start with the realistic monthly rent the property can bring in based on market conditions, condition, and location.

🏦 Financing Costs

Mortgage payments often form the biggest monthly expense, especially on financed rental properties.

🏛 Taxes & Insurance

Property taxes and insurance can significantly change the deal once they are added to the monthly budget.

🧰 Maintenance & Repairs

Even good rentals need ongoing upkeep, repairs, and reserve planning over time.

📉 Vacancy Buffer

A realistic cash flow estimate should include some buffer for vacancy, turnover, or non-payment risk.

🎯 Net Monthly Result

The real question is what remains after all of the likely expenses are subtracted from rental income.

📊 Typical Expenses to Include in Your Cash Flow Estimate

A strong rental analysis includes more than just rent and mortgage. Factoring in all likely monthly expenses helps you avoid underestimating costs and overestimating profit.

🏦 Mortgage

Principal and interest payments based on your loan terms.

🏛 Taxes

Property taxes can significantly affect monthly cash flow in many areas.

🛡 Insurance

Landlord or property insurance based on coverage and risk.

💡 Utilities

Electric, gas, water, sewer, and other recurring services.

🧰 Maintenance

Repairs, upkeep, and ongoing property maintenance.

📉 Vacancy

A buffer for periods when the property may not be rented.

These categories are estimates and should be adjusted based on real property data, local costs, and your investment strategy.

🧮 Estimate Your Monthly Rental Cash Flow

Use this calculator to compare expected monthly rent against common ownership expenses and estimate whether a property may produce positive cash flow.

👉 Many deals look profitable until you add vacancy, maintenance, taxes, and insurance.

Your Estimated Monthly Cash Flow

Total Monthly Expenses: $0

Estimated Monthly Cash Flow: $0

Now that you have a rough estimate, the next step is making sure the financing and protection side of the deal still make sense.

🏦 Stress-Test the Deal With Better Financing Options

If your projected cash flow feels tighter than expected, financing terms may be one of the biggest levers in the deal. A different rate, loan structure, or financing path can change the monthly picture.

Comparing financing options can help you understand whether the property still works for your strategy.

🏦 Compare Financing OptionsRates, terms, and approval options vary by lender and borrower profile.

🚀 What Do You Want to Do Next?

Estimating rental cash flow is one of the smartest ways to evaluate whether a property actually fits your strategy. The more clearly you understand the income, expenses, financing, and monthly profit, the easier it becomes to make a confident decision.

Before moving forward, it can also help to review your repair budget, monthly ownership costs, and financing options together — not separately.

Want help reviewing a deal or planning your next step? Reach out and I can help you evaluate it.

Welcome Home Network LLC helps connect buyers, investors, and homeowners with real estate opportunities across South Jersey.